The prospect of trying to find a mortgage when you have got poor credit may cause folks quite a lot of nervousness. Chances are you’ll assume that due to your poor credit score historical past, no financial institution would ever lend you the cash. So why even apply? Nicely, what if we instructed you that no matter your credit score historical past, many lenders are prepared to mortgage YOU cash? It’s true! And in the present day we’ll be instructing you all about learn how to discover poor credit house loans.

On this article, we’re going to cowl what that you must know to get accepted with poor credit:

- How credit score scores are calculated and how one can shortly enhance your quantity

- What the debt-to-income ratio is and why lenders use this indicator

- Who qualifies for FHA loans and different packages obtainable for house consumers

Don’t waste one other second permitting your credit score rating to maintain you away from the magical feeling of homeownership.

Discover assets for poor credit house loans by state and by metropolis!

We Can Assist You Get Certified Even With Low Credit score

Fill Out The Type Under To Get Assist At this time! Article continued after type

Discovering a lender to present you a mortgage with a low credit score rating is our specialty. Nonetheless, you’re going to run into some points that it’s vital to find out about forward of time.

When your credit score rating dips under the typical mark of 620, to assist shield the financial institution’s preliminary funding, many lenders could require:

- Increased Down Funds

- Mortgage Insurance coverage

- Increased Curiosity Charges

The distinction of even just a few factors might have a main impression on the amount of cash it can save you on a mortgage.

Because of this we extremely encourage you to educate your self in your credit score rating.

In the long term, the next credit score rating might prevent 1000’s of {dollars}.

Compensating Components to Overcome a Low Credit score Rating

It’s no secret that your credit score rating is extraordinarily vital to lenders who take into account issuing you some kind of house mortgage. Your creditworthiness offers the lender some safety; you might be prone to pay again your private home mortgage in full. A low credit score rating might point out that you just’re extra prone to default in your mortgage.

To make up for the chance, many lenders will supply potential house consumers the chance to give you compensating components.

Down Fee

Everyone advantages from it at the very least for a while

The most typical compensating issue is the down fee. Historically, lenders have required a twenty p.c down fee for typical mortgage packages. Should you have been to have a look at the numbers, because of this you would want $20,000 for a $100,000 house.

It’s a approach for the lender to make sure that they’ve some safety if debtors go into default on their poor credit house loans. When the house strikes into foreclosures, the financial institution can relaxation assured that they are going to recoup a good portion of their cash because of this good-looking down fee.

In case you have a low credit score rating, lenders could require a bigger down fee upfront to attenuate their general danger. This compensating issue will apply to traditional mortgage loans. Additionally, FHA loans for poor credit, VA loans, and different kinds of house mortgage merchandise require some down fee.

How a lot must you plan to place down should you’re a first-time purchaser with poor credit? Sadly, there isn’t a one-size-fits-all reply in the case of a down fee that might make up for poor credit score. The thought is solely that you should have extra fairness within the house, which is healthier for the monetary establishment who’s loaning you the cash. It’s best to plan to have a reasonably sizeable down fee in the case of poor credit house loans although.

Mortgage Insurance coverage

So typical and so interesting

Along with a bigger down fee, lenders could require mortgage insurance coverage for a first-time purchaser with poor credit or every other sort of poor credit house loans. This sort of insurance coverage is usually known as PMI (personal mortgage insurance coverage), and its main function is to shield the lender.

Mortgage insurance coverage is usually required on all typical house loans which have a down fee decrease than twenty p.c. It lowers the general danger to a lender, however it additionally will increase the month-to-month value of your private home.

The typical fee for personal mortgage insurance coverage varies based mostly on the general mortgage quantity. Usually, the fee will vary wherever from 0.3 p.c to 1.5 p.c of the house’s whole value annually.

How does that translate into real-world numbers?

Should you bought a house on the nationwide common worth of $203,000, your mortgage insurance coverage might value wherever from $609 to $3,045 yearly ($50.75 to $253.75 monthly). This can be a vital value that would put some properties properly outdoors the realm of what’s inexpensive for potential consumers.

In some circumstances, you might be able to get the personal mortgage insurance coverage eliminated as soon as sufficient fairness is constructed up within the house. The main points in your mortgage could differ, however some monetary establishments will permit householders to request the cancellation of PMI once they have the equal of a twenty p.c down fee invested into the home.

Some packages, just like the FHA loans for poor credit and others for a first-time purchaser with poor credit, could require mortgage insurance coverage all through the mortgage. Whereas this can be a vital month-to-month value, it does let you personal your very own residence as a substitute of lease.

Credit score Scores

Do you ever marvel precisely what your lender is speaking about once they begin mentioning your credit score rating? Even a lease to personal for poor credit could reference this elusive quantity. However just a few folks actually perceive what it means or the place it comes from. Earlier than you are able to do any work in your credit score rating, you must know what this all-important quantity means and the way it’s calculated.

How Do They Come Up with Credit score Scores?

Have a look at the statistics and you can be extra ready

A credit score rating is one of the best ways lenders can choose your general monetary well being. It features a complete look at each essential space that impacts your long-term funds.

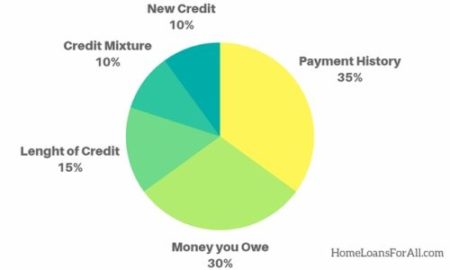

Many lenders are literally your FICO credit score rating earlier than figuring out whether or not you qualify for poor credit house loans. This quantity is decided via sophisticated calculations that weigh 5 main areas associated to your monetary well being:

- Your fee historical past (35%)

- Sum of money you owe (30%)

- The size of your credit score historical past (15%)

- Your credit score combination (10%)

- New credit score (10%)

Every of those classes is weighted barely otherwise in the case of calculating your general credit score rating. You may see the precise illustration of the standard percentages within the parentheses that comply with. Nonetheless, these numbers might differ barely relying in your precise credit score historical past.

For instance, first-time consumers with poor credit could not have an extended credit score historical past which can shift the general weight of every class considerably.

It ought to be famous that your credit score rating is far totally different than the extra simplistic credit score report. You’re entitled to a free credit score report from every of the three main credit score reporting bureaus annually (Equifax, Transunion, and Experian). These reviews are designed to element your precise fee historical past together with any occasions the place you have been late on funds or missed them altogether.

As compared, your credit score rating takes this data into consideration however balances it with different key particulars. It’s a straightforward approach for lenders to rank your monetary well being in comparison with different shoppers who’re additionally making use of for a traditional mortgage or poor credit house loans.

The knowledge contained inside your credit score report is a figuring out issue for calculating your general credit score rating. Chances are you’ll uncover that you’ve got a number of credit score scores and that every one is barely totally different. It’s because every credit score reporting company might have totally different data relating to your historical past.

What’s a Unhealthy Credit score Rating?

Lenders decide in your creditworthiness based mostly on the ultimate quantity assigned to your monetary historical past. The credit score rating score scale usually runs from 300 factors to 850 factors, although you may even see some variation relying on the precise scale used. It doesn’t matter what, the next quantity represents a greater credit score rating.

There may be by no means a credit score rating too dangerous! You may at all times enhance it!

To find out how a lender would fee your credit score rating, you’ll be able to see which of those brackets you fall into. These are the overall pointers that many monetary establishments will use to find out the charges related together with your mortgage or any sort of poor credit house loans.

- Unhealthy: 300 to 499

- Poor: 500 to 579

- Low: 580 to 619

- Common: 620 to 679

- Good: 680 to 699

- Glorious: 700 to 850

A better credit score rating comes with extra favorable phrases and merchandise obtainable for shoppers. However, a decrease credit score rating (like these seen for poor credit house loans) tends to warrant greater charges and rates of interest for potential house consumers.

When your credit score rating dips under the typical mark of 620, many lenders develop into hesitant to situation a traditional mortgage product. They could require greater down funds and mortgage insurance coverage, or chances are you’ll face greater rates of interest to assist shield the financial institution’s preliminary funding. FHA loans for poor credit are troublesome to seek out for people who’ve a credit score rating under 620.

Debt-to-Revenue Ratio

A debt-to-income ratio (typically denoted as DTI) is one other key measure utilized by lenders to find out the main points of a mortgage product. This quantity is an indicator that compares your general debt to the quantity of revenue you have got every month. Lenders are in the end trying to find people who’ve a decrease ratio. Small DTI demonstrates an awesome stability and means you usually tend to pay payments in a well timed method.

How do you calculate your debt-to-income ratio? The calculation is definitely fairly easy when you have a great deal with in your month-to-month payments and debt.

Seize a calculator and a stack of your month-to-month payments to tally up the whole quantity of recurring month-to-month money owed you have got (together with pupil loans, auto loans, bank card debt, and every other cash you have got borrowed). Divide this quantity by your gross month-to-month revenue and multiply the reply by 100.

Are you good at maths?

This offers you an general share that tells you ways a lot of your obtainable revenue is used to pay down your debt on a month-to-month foundation.

To offer you an instance utilizing real-world numbers, let’s suppose that your month-to-month debt incurs payments that seem like these:

- Pupil loans: $400 monthly

- Auto Mortgage: $250 monthly

- Bank card debt: $180 monthly

- Private mortgage: $120 monthly

Altogether, you pay roughly $950 monthly to cowl the price of the cash you borrowed up to now. Suppose that your gross month-to-month revenue is $3,500 {dollars}. While you divide $950 by $3,500 and multiply by 100, you can see a debt-to-income ratio of roughly 27 p.c.

What’s Unhealthy Debt-to-Revenue Ratio?

As soon as what your debt-to-income ratio really is, it’s cheap to marvel what share is taken into account “dangerous” by lenders. This is a vital issue for acquiring a mortgage for a first-time purchaser with poor credit or any sort of poor credit house loans. In spite of everything, research have proven that people who’ve the next ratio usually tend to battle with paying their month-to-month payments.

Most lenders will seek for debtors with a DTI of lower than 43 p.c.

This debt-to-income ratio will be calculated each with and with out the brand new mortgage you’re making use of for. If it consists of your preexisting debt together with the possible poor credit house loans, lenders usually wish to see a ratio underneath 45 p.c. They could be inclined to nonetheless situation a mortgage if there are compensating components.

Lenders should make sure that you’ll nonetheless manage to pay for left on the finish of the month to cowl on a regular basis incidentals that aren’t factored into this ratio. These can embody your utilities, telephone invoice, web invoice, groceries, and gasoline to your automotive. With out cash left over, you received’t be capable of cowl these prices and are prone to default on at the very least one among your different funds.

Unhealthy Credit score Mortgage Loans

You’ve accomplished the analysis and also you already know that you’ve got poor credit score. Maybe you filed for chapter up to now otherwise you had a house transfer into foreclosures. Apart from engaged on bettering your credit score historical past, you continue to have loads of choices for poor credit mortgage loans. Whether or not you reside in New York or California or wherever between, you must look into authorities packages to find out should you meet the necessities.

There are three main authorities packages that supply poor credit mortgage loans to people with poor credit. These three heroes are FHA loans for poor credit, VA loans, or USDA loans. You should decide with of those poor credit mortgage loans is likely to be best for you:

- FHA Loans: These house loans are greatest for people who need a particularly low down fee however don’t thoughts paying mortgage insurance coverage all through the mortgage.

- VA Loans: VA loans include no down fee and low-interest charges, however you have to be a veteran with a view to qualify.

- USDA Loans: These poor credit mortgage loans are ideally suited for individuals who wish to buy a house in a rural space with little to no down fee, however they are going to require a barely greater credit score rating.

FHA Loans

Federal Housing Administration? Somewhat Truthful House Loans Administration!

The FHA loans for poor credit are assured partially by the Federal Housing Administration. This system is designed to make lenders really feel safer. They’re extra prepared to situation loans to people who’ve poor credit, first-time house consumers. Should you default on the mortgage, the federal authorities will assist to cowl the price of the default to your personal lender.

These poor credit house loans all have one very outstanding benefit that first-time consumers with poor credit ought to pay attention to.

Low Down Fee

A low down fee is pretty common on FHA loans for poor credit. This one attribute is what makes many first-time consumers with poor credit flock to this particular authorities program. Chances are you’ll pay as little as 3.5 p.c in a down fee with a FICO credit score rating of 580 or greater.

If you’ll find a lender prepared to situation FHA loans for poor credit, people with decrease credit score scores should still be capable of qualify with a barely bigger down fee. Decrease credit score scores typically require a ten p.c down fee. This decrease down fee gives a superb alternative for people and householders to economize.

Figuring out how a lot it can save you is a bit difficult, so we’ll check out some actual numbers. The typical sale worth for a house in america is roughly $200,000. A standard mortgage product would require a $40,000 down fee. By comparability, a 3.5 p.c down fee would equate to $7,000, and a ten p.c down fee would equal $20,000.

Householders might save as much as $33,000 on this state of affairs by selecting to go together with FHA loans for poor credit.

Saving up for the down fee on a brand new house is commonly probably the most time-consuming a part of the method for potential consumers. It may possibly take years to scrape collectively sufficient financial savings to withdraw $40,000 out of your checking account. By comparability, the FHA loans for poor credit make the preliminary necessities considerably extra accessible.

FHA Necessities

Many lenders make the most of the identical basic pointers to qualify potential consumers for these poor credit house loans. Nonetheless, you must take into account that the precise necessities could differ barely relying on the lender.

Many lenders make the most of the identical basic pointers to qualify potential consumers for these poor credit house loans. Nonetheless, you must take into account that the precise necessities could differ barely relying on the lender.

Apart from a down fee that ranges from 3.5 to 10 p.c based mostly in your credit score rating, you need to additionally meet these necessities.

- Debt-to-Revenue Ratio

You need to meet sure debt-to-income ratio numbers with a view to qualify underneath many of the FHA loans for poor credit.

Your front-end debt-to-income ratio (mortgage fee, insurance coverage, property taxes, and personal mortgage insurance coverage) ought to equal 31 p.c of your gross month-to-month revenue. Lenders could approve a mortgage for candidates who’ve a front-end DTI of as much as 40 p.c when you have some compensating components.

Your back-end ratio (all month-to-month debt funds plus the price of the brand new mortgage) ought to be 43 p.c or much less of your whole month-to-month revenue. Just like your front-end DTI, some lenders will approve greater back-end ratios of as much as fifty p.c with compensating components.

- Credit score Rating

Most lenders would require a credit score rating of 500 or greater to qualify you for FHA loans for poor credit. Nonetheless, that is really decided on a case-by-case foundation by every particular person lender that provides FHA loans for poor credit. They’ll weigh your credit score historical past and any potential bankruptcies or foreclosures to find out if there have been extenuating circumstances past your management. With a purpose to obtain the most quantity of financing, you need to have a credit score rating of 580 or greater.

Decrease credit score scores within the 500 to 579 vary will normally require a ten p.c down fee at minimal.

In contrast to some typical merchandise, you’ll be able to settle for a financial reward from a member of the family to cowl the preliminary down fee.

- Property Necessities

The property necessities for FHA loans for poor credit are literally comparatively easy to adjust to. Every potential house should have a present appraisal and inspection to make sure that it complies with minimal property requirements associated to well being and security. For instance, your appraisal ought to embody the situation of things corresponding to:

- Plumbing

- Electrical energy

- Septic programs

- Basis points

- HVAC system functioning

If the house can not meet requirements that might indicate that’s good to your well being and security, these FHA loans for poor credit can be derailed indefinitely. The house should even be used as your main residence.

- Mortgage Insurance coverage

It ought to be famous that FHA loans for poor credit would require personal mortgage insurance coverage all through the period of the mortgage, notably should you had a down fee decrease than ten p.c. This may add as much as a major value over the thirty-year period of most FHA loans for poor credit.

A $200,000 house might require annual mortgage insurance coverage starting from $600 to $3,000. At this fee, you’d be paying a further $18,000 to $90,000 over the course of a thirty-year mortgage.

Householders who put down ten p.c or extra in direction of their poor credit house loans could qualify to take away their mortgage insurance coverage after eleven years. Many first-time consumers with poor credit could wish to take into account rising their financial savings with a view to qualify for this vital benefit.

The FHA program is a superb choice for people who want poor credit house loans. The low down fee could make homeownership a extra rapid actuality regardless of the necessity for mortgage insurance coverage every month.

VA Loans For Unhealthy Credit score

A VA mortgage is a singular poor credit house mortgage choice obtainable via personal lenders that options authorities backing. A portion of every mortgage is assured by the Division of Veterans Affairs for eligible people. Very similar to the FHA loans for poor credit, lenders are extra apt to contemplate candidates who wouldn’t qualify for a extra conventional mortgage program.

The federal authorities will insure a selected portion of the mortgage (normally as much as $36,000) for eligible service members if the client defaults on the mortgage. There are vital benefits that include a VA mortgage, even these issued as poor credit house loans for eligible people and households.

There are vital benefits that include a VA mortgage, even these issued as poor credit house loans for eligible people and households.

Maybe probably the most vital perk of this program is that lenders could not require any down fee in any respect. Personal mortgage insurance coverage premiums are additionally waived for these poor credit house loans.

Easy benefits of those mortgage packages can save potential consumers 1000’s of {dollars} over the course of their mortgage time period. That is what makes them ideally suited as poor credit mortgage loans for individuals who qualify.

Can you qualify for these favorable house loans? Fewer people qualify for this program since you should meet particular pointers relating to service within the armed forces. You will discover out extra concerning the particular necessities under.

No minimal credit score rating

VA loans are nice poor credit house loans for people who’ve poor credit. The federal authorities doesn’t specify a minimal credit score rating with a view to again the mortgage with a non-public lender. As a substitute, they encourage lenders to take a more in-depth take a look at every utility and take into account your data on a case-by-case foundation.

You might qualify even should you’re a first-time purchaser with poor credit or no credit score.

Every lender could set out their very own credit score rating standards to situation loans to potential consumers. The usual benchmark for a lot of lenders is a credit score rating of 620, however there are many choices for people with decrease credit score scores as properly. Lenders usually tend to take a danger on less-qualified candidates due to the backing of the federal authorities.

The federal government has no particular credit score necessities, which suggests they are going to insure a portion of the mortgage so long as you discover a lender who will work with you. Should you face rejection at one monetary establishment for these poor credit house loans, don’t surrender. You may at all times apply elsewhere with one other alternative for fulfillment.

Acquiring Your Certificates of Eligibility

A VA mortgage is a superb choice for people and households who want poor credit house loans, however you need to meet a stringent set of standards to qualify. Lenders would require you to acquire a Certificates of Eligibility based mostly on the period of time you have been enlisted in a department of the armed forces. Relying on the time interval and the variety of years you spent in service, these necessities will be difficult to calculate.

For extra data relating to the standards to qualify for a certificates of eligibility, you’ll be able to verify the service necessities right here.

USDA Unhealthy Credit score House Loans

Do you dream of proudly owning a house within the nation? In that case, a USDA house mortgage could show you how to to make your desires right into a actuality. These house loans are backed by america Division of Agriculture to encourage householders to buy properties in eligible rural and suburban areas.

Just like the VA loans and FHA loans for poor credit, the USDA typically backs a portion of the mortgage. In flip, personal lenders usually tend to grant approval for loans to potential consumers who don’t meet their customary standards.

In contrast to the FHA loans for poor credit, chances are you’ll qualify for a direct mortgage from the Division of Agriculture. Candidates who obtain one of these direct mortgage usually have very low to low month-to-month incomes, although the precise necessities will differ based mostly in your location.

Among the best options of a USDA mortgage is the foremost financial savings it could entail for potential consumers. Many eligible properties could let you make a purchase order with no down fee or with a really minimal down fee, relying on the specifics of your mortgage.

Increased Credit score Rating Required

Sadly, USDA loans do require a barely greater credit score rating than the FHA loans for poor credit. Many lenders will wish to see a regular 640 credit score rating or greater with a view to obtain extra streamlined processing of your mortgage. That doesn’t essentially imply that you just received’t obtain funding underneath this program.

Candidates who’ve a credit score rating underneath the 580 mark should still be capable of obtain one among these mortgages. Candidates who’ve the next credit score rating are normally topic to automated underwriting, however it isn’t the one choice. A decrease credit score rating merely signifies that you’ll have to undergo guide underwriting to find out if you’re eligible to obtain one among these poor credit house loans.

Throughout guide underwriting, an precise individual will assessment the main points positioned in your credit score historical past and utility. Whereas this will decelerate the general course of, chances are you’ll discover that it really works out in your favor. Your private data has the eye of an actual one who can take extenuating circumstances into consideration.

This additionally signifies that your approval shall be extremely subjective. The place one lender could agree that you must qualify, one other should still flip down your utility for poor credit house loans. Don’t be discouraged by these discrepancies. As a substitute, you have to to proceed to strive at different monetary establishments that could be inclined to take a larger danger.

USDA finally desires you to maneuver out of city and develop into a great neighbor within the suburbs. Individuals of sure professions, like nurses, academics, policemen, are very a lot welcome to make use of USDA. Good neighbors are at all times welcome wherever.

Compensating Components

In case you have a decrease credit score rating, your underwriter is probably going to try different compensating components to find out your eligibility. Many owners could also be required to give you easy gadgets corresponding to a bigger down fee that would decrease the general month-to-month value of your mortgage.

In different situations, they might take a look at what money reserves you should have left following your official closing ceremony. Lenders wish to see a number of months’ price of mortgage funds remaining in your checking account. To a lender, because of this they’re assured a larger probability of receiving your month-to-month mortgage fee even when you have some extenuating circumstances or surprising payments that month.

They could additionally take into account whether or not you might be assured to obtain a promotion or increase within the close to future. When month-to-month revenue is anticipated to extend, it could dramatically alter your debt-to-income ratio and make you a extra interesting applicant.

A guide underwriter can even take into account what you might be at the moment paying your lease or mortgage compared to the house you wish to buy with a USDA mortgage. Month-to-month funds that may stay comparatively steady will exhibit you could deal with the monetary burden this new mortgage might impose. With a purpose to decide should you can responsibly deal with the change, they are going to take a look at your credit score historical past and measure what number of lease or mortgage funds you have got issued on time.

Lease to Personal Choices

A lease to personal is an interesting choice for a lot of potential consumers who could not qualify for any poor credit house loans within the current second. They will transfer into a house proper now whereas they make modifications that enhance their general credit score rating. First-time consumers with poor credit who’re desirous to make a home into a house could wish to examine one among these choices for lease to personal with poor credit.

How Does It Work?

Many house consumers are questioning how this lease to personal state of affairs works. With a purpose to provide the greatest thought of what a lease to personal with poor credit will actually seem like, we’re going to contemplate it with some real-world numbers.

You’ll begin wanting round for properties which are supplied underneath this class. You might be able to discover them via a neighborhood actual property agent, the newspaper, or through on-line listings. The month-to-month value is normally similar to what you’d pay in lease or for a brand new mortgage, however a few of this lease really goes towards the acquisition worth of the house.

Let’s suppose that the house you discover is price the identical as a mean house worth in america at roughly $200,000. Which means that your lease fee could possibly be in a variety of $1,200 to $1,800 monthly, relying on the world you reside in and what’s included in your lease.

Of this month-to-month lease fee, a small portion shall be put aside to go towards the acquisition worth of the house. It will differ based mostly in your particular contract, however it could be $200 to $400 monthly.

Along with your month-to-month lease fee, a lease to personal for poor credit normally requires an choice charge. Which means that you should have the choice of buying the house as soon as the contract is over in just a few years. Just like a down fee, this selection charge will normally be a number of thousand {dollars} and signify a good portion of the acquisition worth of the house.

Professionals

Clearly, there are a number of benefits to deciding on lease to personal for poor credit eventualities. Essentially the most engaging choice for one of these buy is you could transfer into the house instantly as a substitute of ready a number of years to qualify for a mortgage. Through the time you reside there, you’ll be able to dedicate your self to sharpening your credit score rating to qualify for a mortgage or extra favorable phrases.

The opposite main good thing about a lease to personal for poor credit is {that a} portion of your lease is put aside towards the acquisition worth of your private home. This can be a assured quantity every month that doesn’t differ based mostly on the quantity of discretionary revenue you have got left on the finish of the month. It may possibly assist to decrease the acquisition worth of the house as a result of it’s a kind of pressured financial savings account for people who lease to personal with poor credit.

As a result of the housing market is consistently altering, a lease to personal for poor credit means that you can lock within the worth based mostly on the present market worth. If financial indicators are displaying that the housing market is prone to enhance over the approaching years, it may be a good time to lock in a superb worth.

Cons

Together with the entire benefits of a lease to personal for poor credit, you should still discover just a few drawbacks when in comparison with poor credit house loans. The obvious drawback to this state of affairs is the massive upfront choice charge to buy the house in years to return. Just like saving up for a big down fee, it could take first-time consumers with poor credit a while to scrape up the cash required.

There may be additionally sure to be some uncertainty over whether or not you’ll really qualify for a mortgage when the settlement is up.

Should you do determine to maneuver ahead with the lease to personal for poor credit and qualify for a mortgage, there’s a chance you may face greater rates of interest. The market charges are consistently fluctuating, so it may be troublesome to foretell the place the charges shall be in 5 years or so. That is an inherent danger of signing the contract for a lease to personal property.

Foreclosures occur. If the proprietor of the house defaults on the present mortgage, you may nonetheless be pressured to depart. If this occurs, you may lose the entire cash you place down for the upfront choices charge and the cash put aside on a month-to-month foundation.

Equally, you’ll lose all of this cash should you determine to terminate the contract with the proprietor. Chances are you’ll notice that this isn’t the suitable house for you after you progress in or chances are you’ll determine that isn’t as inexpensive as you as soon as thought. It doesn’t matter what the explanation, contract termination of a lease to personal for poor credit will value you a reasonably penny.

What to Look For

While you search for lease to personal with poor credit, you continue to want to make sure that you’re searching for the suitable sort of property to your wants. A very powerful factor to seek for is a house that you’ll be able to afford long-term. Should you train your proper to buy a lease to personal for poor credit, you have to to make the mortgage fee on time every month. An inexpensive house could also be an important consideration a potential purchaser can actually search for.

Nonetheless, you also needs to confirm that the property is totally free and away from any liens. Within the occasion that the proprietor doesn’t at all times make well timed funds, one other firm could have positioned a lien towards the house. This could be a headache when it comes time to switch the property out of your lease to a brand new mortgage.

Potential consumers for a lease to personal with poor credit have to have a transparent contract with the proprietor of the property. It ought to spell out all monetary obligations of each events, your particular choice to buy on the finish of the lease, and the parameters of your funds.

Don’t get too excited a few particular lease to personal for poor credit till you have a house inspection carried out on the property. This might help you to determine any main structural points and provide the proper to start negotiating the property worth based mostly on these essential repairs. An inspection can even provide you with some data to assist decide whether or not this specific lease to personal for poor credit is priced at truthful market worth.

Cosigner on a Unhealthy Credit score Mortgage

Co-signer = TRUST

In case your credit score isn’t ok to qualify for a mortgage by yourself, a cosigner might be able to provide you with a much-needed enhance. Your co-signer doesn’t have to really reside within the property with a view to show you how to qualify for a brand new mortgage. Nonetheless, they’re putting their credit score on the road to your mortgage.

A possible lender will pull the credit score for each the occupant and the cosigner. Your cosigner’s title and credit score rating develop into tied to the mortgage, for higher or worse. Late or missed funds will present up as a blemish on the cosigner’s credit score report. Moreover, they might be on the hook for making funds should you miss them.

The stipulations on cosigning will differ based mostly on the precise sort of mortgage you apply for. We are going to take a more in-depth take a look at two of the extra frequent poor credit house loans.

Typical Mortgages

If you’re making use of for a traditional mortgage with a cosigner, each of your credit score scores shall be assessed to find out eligibility. Debt-to-income ratios will differ based mostly on each your quantity and your cosigner’s quantity. For instance, the one that will bodily occupy the property could have a debt-to-income ratio of as much as 70 p.c. The cosigner’s required debt-to-income ratio will differ.

A standard mortgage with a cosigner would require the cosigner to signal the precise mortgage itself, however their title doesn’t have to be on the title.

FHA Loans

The key distinction between typical mortgages and FHA poor credit house loans with a cosigner is the property title. Your cosigner shall be on each the mortgage and the title of the property. You will have as much as two non-occupying cosigners on the mortgage itself.

The credit score scores of each the applicant and the cosigners will nonetheless be pulled for FHA loans for poor credit. The utmost debt-to-income ratio shall be similar to that required for a traditional mortgage on this state of affairs.

There are additionally particular necessities relating to who can develop into a cosigner on FHA loans with poor credit. All potential cosigners have to be both family or shut associates. The friendship have to be documented to show a prolonged relationship. It’s best to present the explanation why they might be desirous about serving to you qualify for a mortgage.

First-time Patrons with Unhealthy Credit score

Are you a first-time purchaser with poor credit? Should you’ve by no means owned a house earlier than, there are numerous packages designed particularly for you. FHA loans are among the finest choices on the mortgage market to help first-time consumers with poor credit in the case of the acquisition of a brand new house.

As a result of the federal authorities is prepared to insure a portion of your private home mortgage, lenders usually tend to take a danger on first-time consumers who don’t have a confirmed document of success. They could be extra apt to grant loans to shoppers who’ve low credit score scores or no credit score in any respect.

Compensating Components

Most FHA loans for poor credit would require a credit score rating of 580 or greater, however some lenders are prepared to look past the numbers. A better credit score rating will usually provide you with extra advantages, corresponding to a decrease down fee of three.5 p.c. Nonetheless, lenders will typically permit for compensating components when you have poor credit score.

- Excessive Down Fee

A down fee has been used traditionally to present lenders some peace of thoughts in case you default on the mortgage. With some small quantity of fairness within the property, they’ve some assure that they are going to be capable of regain a portion of their funding if the house strikes into foreclosures. In case you have a decrease credit score rating, the chance of defaulting on the mortgage is far larger and plenty of lenders could also be hesitant to take the chance.

FHA loans for poor credit are normally chosen as a result of they characteristic a particularly small down fee quantity of simply 3.5 p.c of the acquisition worth. Nonetheless, people with decrease credit score scores or first-time consumers with poor credit could face the next required down fee. Scores lower than 580 will warrant a 10 p.c down fee in your new house.

Despite the fact that this would be the minimal requirement, the next down fee will proceed to weigh in your favor. The extra money it can save you as much as place down on a brand new house, the extra probably a lender shall be to situation a mortgage to first-time consumers with poor credit or no credit score in any respect.

- Massive Financial savings Account

As vital as your down fee is, your financial savings account could possibly be equally vital. Lenders don’t wish to see you empty out your total nest egg with a view to meet the minimal necessities for a down fee. An underwriter can even be looking at your financial savings account to make sure that you have got cash in reserve after the closing is over.

Your money reserves are form of like a security web for lenders. Notably when you have the next debt-to-income ratio, one surprising invoice for the month might imply the distinction between paying your mortgage and lacking it. Automobile repairs, an exorbitant cellphone invoice or a medical emergency can all pop up at a second’s discover.

In case you have cash in your financial savings account, you’re extra prone to proceed making the mortgage funds. Many lenders favor to see roughly six months’ price of bills in your financial savings account to make up for a decrease credit score rating. First-time consumers with poor credit ought to intention to have one of these emergency fund constructed up previous to making use of for a brand new mortgage.

- Excessive Revenue

Do you have got poor credit score however a excessive revenue? This could possibly be one other actual compensating issue that may make you extra engaging to a possible lender. A better revenue could make your debt-to-income ratio seem a lot smaller and provide you with extra wiggle room in the case of making your month-to-month funds.

First-time consumers with poor credit could wish to take into account what share of their revenue a brand new mortgage would require. The smaller that share is, the extra probably a lender shall be to situation you a house mortgage based mostly in your gross month-to-month revenue.

A better revenue may also make it simpler to fulfill a number of the different compensating components corresponding to the next down fee or a big financial savings account. Each of those financial savings varieties will accrue a lot sooner and make you a extra interesting candidate. Even should you occur to fall into the class of first-time consumers with poor credit. Lenders simply love their cash upfront.

- Employment Historical past

No lender desires to situation a mortgage to somebody who has a really spotty historical past of holding a job. Steady and regular employment is a big consider figuring out whether or not you might be eligible for any of the loans obtainable to first-time consumers with poor credit. Lenders are sure to have a look at a number of years’ price of your employment historical past and should even verify your references.

Ideally, they would like to see you’re employed with the identical employer for no less than two years. They could make some exceptions should you switch to a unique firm however keep the identical place. Equally, they might take extenuating circumstances into consideration should you have been let go attributable to inside struggles inside the firm.

Make certain that you have got an extended historical past of displaying as much as work diligently at your scheduled occasions with a view to qualify based mostly on this compensating issue.

Unhealthy Credit score House Loans After Chapter

Many people consider they might by no means be capable of personal actual property once more after declaring chapter. You will have confronted some rocky monetary occasions up to now, notably in an financial downturn. Nonetheless, you should still have an opportunity at homeownership based mostly on pointers established to assist potential consumers qualify following a chapter.

These “second probability house loans” have their very own {qualifications} and eligibility standards. To accommodate the distinctive circumstances that people who filed for chapter could face, all mortgage merchandise now supply particular ready intervals. These ready intervals provide you with time to rebuild your credit score and set up your self financially as soon as extra.

Typically, you’ll be able to anticipate finding these ready intervals of various house loans:

FHA loans:

VA loans:

Typical loans:

USDA loans:

Should you confronted an extenuating circumstance that resulted within the lack of revenue outdoors of your management, chances are you’ll qualify for a brand new mortgage even sooner. Each typical mortgages and FHA loans for poor credit will situation these exceptions. A standard mortgage solely requires a two-year ready interval and an FHA mortgage requires solely a one-year ready interval on this state of affairs.

Foreclosures and Ready Durations

While you expertise a lack of revenue, it may be extraordinarily difficult to make ends meet on a month-to-month foundation. Many properties will transfer into foreclosures to assist decrease month-to-month prices, however that is probably not sufficient to cowl the price of your mortgage. Finally, your lender will wish to search fee for the rest of the stability in your mortgage.

Let’s suppose that you just nonetheless owe $100,000 on the house you bought ten years in the past. You all of a sudden misplaced your job, and the financial institution moved the house into foreclosures. On the public sale, the house could have solely bought for $75,000. Sadly, your lender nonetheless isn’t proud of this $25,000 discrepancy within the worth distinction.

Relying in your state legal guidelines, a lender might be able to file this $25,000 as a deficiency which you’ll nonetheless owe. Many people are unable to cowl the price of the deficiency, in order that they file for chapter to erase the debt.

In different eventualities, a household could file for chapter earlier than the house strikes into foreclosures. Dropping the house could also be part of the chapter course of. The order wherein these processes happen might decide how lengthy you must wait earlier than you take into account homeownership once more sooner or later.

If the foreclosures of your earlier house occurred earlier than you filed for chapter, the ready interval will start from the chapter date.

If the foreclosures of the house occurred after the chapter date, chances are you’ll face totally different ready intervals. For instance, FHA loans for poor credit will then require a three-year ready interval. Typical mortgages will nonetheless let you base the ready interval on the chapter discharge date.

What Can You Do Through the Ready Interval?

Should you’re trapped in one among these lengthy ready intervals, you don’t essentially have to sit down idly and look forward to the times to go. You’ll have a higher probability of receiving a mortgage sooner or later if you’ll be able to take some steps towards actively rebuilding your credit score. It should take quite a lot of exhausting work and dedication, however it’s potential to create a great credit score rating after chapter.

The very best factor you are able to do is open credit score accounts after which persistently pay the invoice every month. A bank card with a decrease most is a good way to observe borrowing cash and repaying it responsibly every month. Remember the fact that lenders favor to see you utilize the credit score restrict responsibly. Most specialists advocate holding your spending to thirty p.c or much less of the obtainable credit score restrict.

You also needs to make an effort to pay your whole payments in a well timed method. This may embody your cellphone invoice, car loans or pupil loans, automotive insurance coverage, or cable. Whereas they might not in the end report these things to the credit score bureau, some lenders will take into account different types of credit score once you apply for a mortgage.

The aim in the course of the ready interval is to ascertain wholesome monetary habits that exhibit your creditworthiness. Make your self a calendar that reveals which payments are due on particular days so that you by no means miss a fee.

Learn how to Enhance Your Credit score Rating

All the time a good suggestion

Bettering your credit score rating is important if you wish to obtain a brand new mortgage or discover extra favorable phrases. You’ll discover advantages that far surpass simply the power to buy a brand new house. Pupil loans, auto loans, and bank card firms are all extra prone to situation you a credit score restrict should you can enhance your credit score rating.

Sadly, many people assume that bettering their credit score rating is simply too difficult. It does take time to undo the injury you wreaked in your credit score, however it isn’t an not possible feat. All that you must do is change a handful of your monetary habits to exhibit to lenders you could be trusted to pay again your mortgage. Habits are exhausting to build-up, however there may be nothing supernatural in that. You are able to do this!

Make Funds on Time

That is maybe one of many best methods to routinely enhance your credit score rating. People who’ve an extended historical past of paying their money owed every month in a well timed method usually have a lot greater credit score scores than those that don’t. Whereas this may increasingly appear extraordinarily troublesome, you must keep in mind that advances in know-how make paying on time simpler than ever.

The only approach to make sure your payments receives a commission every month is to join auto-pay. Most firms supply an auto-draft characteristic via their on-line fee portal. Signing up and providing your checking account data is a fast and simple strategy to ensure you always remember a selected fee once more.

If a few of your payments don’t have this characteristic, chances are you’ll wish to take into account setting an alarm in your telephone. Make it possible for it’s set to recur month-to-month so that you just by no means miss one other fee. It will make it simpler to seek out poor credit house loans sooner or later.

Scale back or Remove Debt

One other easy approach to enhance your general credit score rating is to scale back or get rid of a few of your debt. Lowering your debt makes you a extra engaging prospect to lenders as a result of it lowers your debt-to-income ratio. A decrease ratio makes you much less of a danger to lenders and means that you can qualify for a greater mortgage.

Many individuals with poor credit score may have a number of open bank cards, every with a various stability. You will have a handful of playing cards with comparatively low balances and solely a pair with greater minimal month-to-month funds. Among the best methods to scrub up your credit score rating is to repay a number of the playing cards with decrease balances.

This straightforward maneuver has two advantages. First, it helps to clear a number of the excellent accounts which are generated by your credit score report. Second, it frees up some cash every month so that you can put towards your bigger money owed.

Please take a second to learn our article on learn how to get credit score scores for the very best mortgage charges.

Unhealthy Credit score House Loans Conclusion

Your credit score rating is a major issue for lenders to contemplate when issuing a brand new mortgage. Nonetheless, poor credit score doesn’t essentially exclude you from the prospect of buying your personal house. Weak credit house loans are pretty plentiful if the place to look.

Sadly, poor credit house loans don’t at all times supply probably the most favorable phrases. It’s vital to start out taking some proactive steps to enhance your credit score now so you’ll be able to qualify for higher mortgage merchandise sooner or later. One of many easiest issues you are able to do to your credit score proper now could be to seek out out the place you stand.

Ask for a replica of your credit score report from one of many three credit-reporting companies. Each client is entitled to a free report annually. Understanding your credit score rating and historical past might help you to make smart selections to enhance that quantity within the years forward. Make certain you’re taking the time to assessment the credit score report rigorously, as there are typically errors.

Should you spot an error that could possibly be blemishing your credit score, contact the credit-reporting company and the supply of the error. You might be able to resolve the difficulty shortly and in the end enhance your credit score rating.

Examine the potential for qualifying for one of many authorities packages corresponding to an FHA mortgage for poor credit. They arrive with vital benefits {that a} typical mortgage product has a troublesome time competing with. Particularly, they typically characteristic extraordinarily low down funds which might make homeownership a extra rapid actuality for most people. Additionally, concentrate on potential scams and know your rights when potential credit score restore packages.

Don’t neglect that persevering with to pay down your debt may also supply an enormous enhance to your potential to qualify for a brand new mortgage. Lowering your debt-to-income ratio does make you way more engaging to lenders and lowers the chance of defaulting on poor credit house loans.

In the end, there are many steps you’ll be able to take to start out bettering the percentages of qualifying for poor credit house loans in the present day. You can begin by contacting a number of the native mortgage firms in your space to see whether or not you would possibly meet the standards for one among these authorities packages or another sort of poor credit house mortgage in the present day.

You continue to received questions? We nonetheless received solutions!

FAQ About Unhealthy Credit score House Loans

Are poor credit house loans assured?

Whereas they aren’t assured, we do work with householders who’ve a low credit score rating to assist them discover the right poor credit house loans program. Weak credit mortgage loans such because the FHA mortgage, VA mortgage, and USDA mortgage are all obtainable for people who can qualify.

Can I get a house mortgage with a credit score rating underneath 550?

Sure, you’ll be able to qualify for poor credit house loans with a credit score rating underneath 550. Every lender may have their very own benchmarks and standards for potential candidates, however a decrease credit score rating will typically require extra compensating components. These can embody an extended historical past of regular employment, excessive revenue, or a bigger down fee out of your financial savings account.

Can I get a USDA mortgage with poor credit?

The minimal credit score rating for a USDA mortgage is 640. Nonetheless, you might be able to discover a lender who’s prepared to manually underwrite a mortgage for decrease credit score scores. You will want to have just a few compensating components, which might embody:

- Massive money reserve to pay for a number of months’ price of mortgage and curiosity funds

- Potential for a increase within the close to future

- Related housing fee at the moment

- Low debt-to-income ratio

- Low whole obligation ratio

Can I get a house mortgage after chapter?

Sure, second probability poor credit house loans can be found after a ready interval. The shortest ready interval comes with the FHA Again to Work program and requires you to attend at the very least one 12 months after a foreclosures or chapter discharge. With a purpose to qualify for this program, you need to have had extenuating circumstances that led to your monetary hardship. These circumstances can embody:

- Lack of 25 p.c of your whole revenue or extra

- Laid off or fired from the present place

- Medical situation or incapacity

You need to exhibit that you’ve got moved on from this monetary hardship, established constructive fee historical past for the previous twelve months, and are at the moment financially steady.

How briskly can I increase my credit score rating?

Bettering your credit score can take time since you should construct a historical past of accountable funds and accountable cash administration. Work on diligently paying your month-to-month payments on time every month and decreasing a few of your general debt. These two main steps might help you to attain a decrease credit score rating in time.

What’s the HOPE program?

The HOPE program final gave out funds in 1994, however this program helped to fund grants that made homeownership extra probably for low-income households in public housing. Cash was made obtainable to public housing authorities, resident administration companies, housing cooperatives, and related companies with a view to educate vital expertise corresponding to:

- Job coaching and different actions to extend financial empowerment

- Monetary help program availability

- Rehabilitation of properties

- Resident and homebuyer counseling and coaching

Can I get poor credit house loans with no down fee?

Sure, you’ll be able to safe poor credit house loans with no down fee. Many packages would require some sort of down fee to grant safety to the lender, however authorities packages just like the USDA house mortgage or VA mortgage don’t require a down fee.

Can I get a primary time house consumers mortgage with poor credit?

Sure, first-time consumers with poor credit can nonetheless qualify for a mortgage, notably if the mortgage is one among a number of poor credit house loans. Lenders could also be extra hesitant to situation these loans until there are clear compensating components like a bigger down fee or the next rate of interest.

You may additionally qualify for packages just like the FHA poor credit house loans. These packages are designed to assist first-time consumers with poor credit to obtain a mortgage with a low down fee.

The place can I discover inexpensive credit score counseling?

The US authorities has a web site with a ton of useful data on low value or free credit score counseling in addition to poor credit house loans.

References

House Loans for Single Moms

10 Ideas For Refinancing Your Mortgage in 2020

HUD Permitted Housing Counseling Businesses

Homeownership and Alternative for Individuals In all places (HOPE I)Making House Inexpensive

Unhealthy Credit score House Loans in Chicago

Unhealthy Credit score House Loans in Columbus, Ohio

Unhealthy Credit score House Loans in Virginia

Qualify for a Mortgage with Unhealthy Credit score

First Time House Patrons Information: Dealing With Low Credit score Scores

Unhealthy Credit score House Loans in Washington State

Choice for Getting a House Mortgage After Chapter

Mortgage Attainable with Credit score Issues

Discovering House Loans for Unhealthy Credit score (Sure, You Can)

Private Loans for Individuals with Unhealthy Credit score or No Credit score